By Norm Singleton

Last Friday, President Trump signed an Executive Order instructing federal agencies to take a number of steps to give seniors more choices in the Medicare program. The executive order repeals a Clinton-era rule forbidding any senior who refuses to accept Medicare from enrolling in Social Security. This provision forces seniors who would rather provide their own health care to accept government health care or forego Social Security benefits. Many seniors need Social Security because taxes and inflation make it difficult or impossible to save for their own retirement. The order also instructs the Health and Human Services Department to remove all barriers to private connections in Medicare. This refers to the extent the existing laws and regulations limit seniors’ ability to use their own money to pay for health care. Current law says that a physician who forms a private contract with a senior cannot file any Medicare claims for two years and that seniors are only eligible to write private contracts with certain types of healthcare providers. Campaign for Liberty Chairman Ron Paul championed repealing these restrictions on seniors’ health freedom when he was in Congress. Below is Dr. Paul’s official statement on his Seniors Health Care Freedom Act, which allowed seniors to form private contracts in Medicare and allowed seniors to decline Medicare without losing their Social Security benefits: Mr. PAUL. Mr. Speaker, I rise to introduce the Seniors' Health Care Freedom Act. This act protects seniors' fundamental right to make their own health care decisions by repealing federal laws that interfere with seniors' ability to form private contracts for medical services. This bill also repeals laws which force seniors into the Medicare program against their will. When Medicare was first established, seniors were promised that the program would be voluntary. In fact, the original Medicare legislation explicitly protected a senior's right to seek out other forms of medical insurance. However, the Balanced Budget Act of 1997 prohibits any physician who forms a private contract with a senior from filing any Medicare reimbursement claims for two years. As a practical matter, this means that seniors cannot form private contracts for health care services.

This article was originally published at The Campaign for Liberty.

Read Part 2 of this article here.

Violent unrest in Iraq over the past several weeks have claimed more than 100 lives and left thousands wounded. With a devastated economy, even 16 years after its "liberation" by the US, and with corruption rampant, it's little surprise that people are taking to the streets. But are there other factors involved in this unrest? Is the US trying to overthrow its "ally" in Baghdad?

By Chris Rossini

America's Founders were not perfect angels. They were not omnipotent, or all-knowing. But they understood the ideas of Liberty and the perpetual struggle of humanity against the sewage of power. Freedom of speech? ... Huge! The natural liberty of arming and defending your life and property? ... Huge! The Founders were geniuses for making these the first two in the Bill of Rights. People may not be able to recite the entire Bill of Rights, but they know those first two. The Founders were also extremely educated when it came to the most important issues of all in trying to chain down the beast of government --- Money & War. Money & War go hand in hand. Cicero knew this when he pointed out: "The sinews of war, unlimited money." Government must never be allowed to create its own money. Give it this power and it will create never-ending war in no time. But why would government want never-ending war? Because, as Randolph Bourne pointed out: "War is the health of the state." It is during times of war (or even just the fear of war) that government capitalizes the most. The Founders were very specific that only gold and silver were Constitutional money. Gold and silver are despised by government. Government cannot counterfeit them. It can't create gold and silver out of thin air. Gold and silver cannot prevent all wars.....but they can prevent never-ending wars. The Founders were also smart in giving the power of declaring war to Congress. Take a look at the thinking, and how our ancestors wanted to prevent perpetual war:

James Madison

"In time of actual war, great discretionary powers are constantly given to the executive magistrate. Constant apprehension of war, has the same tendency to render the head too large for the body. A standing military force with an overgrown executive will not long be safe companions to liberty…Throughout all Europe, the armies kept up under the pretext of defending, have enslaved the people." George Washington "The Constitution vests the power of declaring war with Congress. Therefore no offensive expedition of importance can be undertaken until after they have deliberated upon the subject and authorized such a measure." James Wilson "This system will not hurry us into war. It is calculated to guard against it. It will not be in the power of a single man or a single body of men to involve us in such distress, for the important power of declaring war is vested in the legislature at large. This declaration must be made with the concurrence of the House of Representatives. In this circumstance, we may draw the certain conclusion that nothing but our interest can draw us into war."

But alas, these two safeguards (sound money and congressional war powers) would be destroyed.

In 1913, the Federal Reserve would be created (unconstitutionally) by Congress. A central bank now existed to counterfeit as much currency as the government wanted. World War II would be the last time that the U.S. Congress would declare war. It has been perpetual war ever since for America, and everything would be turned upside down. Congress would remain silent. All of a sudden it was up to the President to decide on war, and the media would glorify and promote it to no end. The moment any President would "back down" or put an end to war, Congress (and the media) would lose their minds and throw a collective fit against it. This continues to the present day. When President Trump sent missiles crashing down into Syria, he was praised as a King. The media pointed out the 'beauty' of it all. But when President Trump wisely does the opposite, such as ----

Do you see what President Trump is up against? The American people (in poll after poll) have been against war for decades. Candidates win elections in America by promising peace. No president has followed through on that, of course. It's just known that (even though you're going to keep the wars going) you have to promise peace to get elected. President Trump has the American people on his side and he is continually speaking out against endless wars that have literally bankrupted America. It's not surprising that his movements to stop never-ending war are met with unbelievable resistance and propaganda. It would be foolish to expect that anything else would occur. War is the biggest government program of them all. It is also the biggest destroyer of life on Earth. Stand strong Mr. President. You couldn't have picked a bigger enemy.

No sooner did President Trump Tweet his determination to remove US troops from the "endless" war in Syria than the entire Washington Beltway had a total breakdown. From Mitch McConnell to Ilhan Omar the cry was identical: "How dare you! How dare you bring US troops home!" Will the President cave in to his enemies in Washington and the media? Or will he keep his promises and fulfill the wishes of a majority of Republicans?

By Ron Paul

Since September 17, the Federal Reserve Bank of New York has pumped billions of dollars into the repurchasing (repo) market, the first such intervention since 2009. The Fed has announced that it will continue to inject as much as 75 billion dollars a day into the repo market until November 4. The repo market provides a means for banks that are temporarily short of cash to obtain short-term (usually one day) loans from other banks. The Fed’s interventions were a response to a sudden cash shortage that caused interest rates for these short-term loans to climb to 10 percent, far above the Fed’s target rate. One of the factors blamed for the repo market’s cash shortage is the Federal Reserve’s sale of assets it acquired via the Quantitative Easing programs. Since launching its effort to “unwind” its balance sheet, the Fed had reduced its holdings by over 700 billion dollars. This seems like a large amount, but, given the Fed’s balance sheet was over four trillion dollars, the Fed only reduced its holdings by approximately 18 percent! If such a relatively small reduction in the Fed’s assets contributed to the cash shortage in the repo market, causing a panicked Fed to pump billions into the market, it is unlikely the Fed will be continuing selling assets and “normalizing” its balance sheet. Another factor contributing to the repo market’s cash shortage was a major sale of US Treasury securities. Sales of government securities leave less capital available for private sector investments, increasing interest rates. This “crowding out” effect provides one more justification for the Federal Reserve to pump more money into the markets. The crowding out effect is just one way federal debt increases pressure on the Fed to keep interest rates low. Increasing federal debt increases pressure on the Fed to maintain low interest rates to keep the federal government’s interest payments from reaching unsustainable levels. The over one trillion dollars (and rising) federal deficit is the major reason the Federal Reserve is likely to keep interest rates low or even adopt the insane policy of negative interest rates. The American people are not even allowed to know what banks benefited from the Fed’s intervention in the repo market, or what plans the Fed is making for future bailouts — even though the people will pay for those bailouts either through increased taxes, debt, or the Federal Reserve’s hidden inflation tax when the next crash occurs. Of course, the average people who will lose their savings and their jobs in the next crash will not be bailed out. This is one more reason why it is so important Congress takes the first steps toward changing monetary policy by passing Audit the Fed. The need for the Fed to shove billions into the repo market to keep that market’s interest rate near the Fed’s target shows the Fed is losing its power to control the price of money. The next crash will likely lead to the end of the fiat money system, along with the entire welfare-warfare state. Those of us who understand the Fed is the cause of, not the solution to, our problems must redouble our efforts to educate our fellow citizens on sound economics and the ideas of liberty. This way, we can create the critical mass necessary to force Congress to cut spending, repeal the legal tender laws to restore a free market in money, and audit, then end, the Fed.

President Trump has indicated that he will fulfill one of his central campaign promises - to get the US out of the endless wars in the Middle East and elsewhere. He has directed US troops to begin withdrawing from parts of northeast Syria in advance of an expected Turkish incursion into the region. Neocons screech that this will mean a comeback for ISIS and that abandoning the Kurds is treachery. They want to continue the "successful" Obama policy of eight years.

Rent controls are one of those zombie government interventions that, no matter how much destruction they’ve caused, seem to never go away. Rent controls may ‘feel good,’ and ‘get votes,’ but they produce very bad consequences. AOC is pushing yet another terrible idea: national rent controls.

No wonder the Democrats wanted a really fast House impeachment vote. As more information comes out about the "whistleblower" and the role of House Democratic leadership to husband the gossip into a complaint - and from there to impeachment - the more it looks like another Steele Dossier. Will this farce blow up in their faces, or will their allies in the mainstream media be capable of keeping any counter-evidence from the screens of mainstream media watching America?

By David Stockman

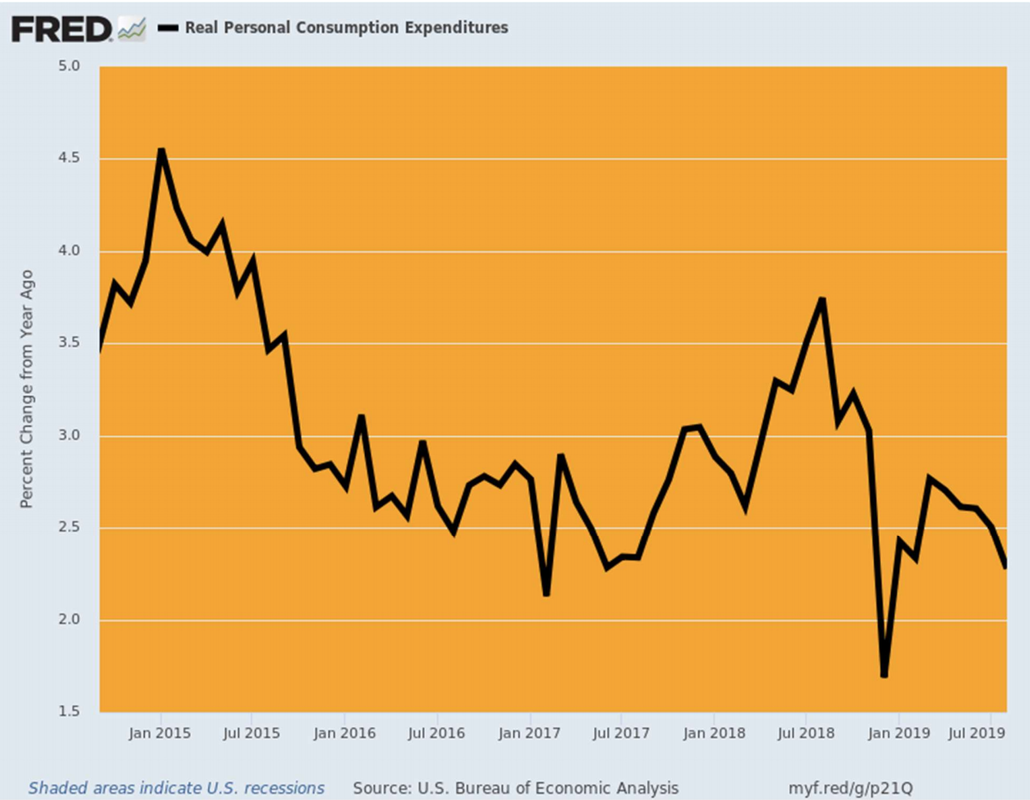

Here is the broadest picture of the American consumer and it sure looks like there's more dropping than shopping going on. So if personal consumption spending (PCE) is the great 70% engine that's supposed to keep the GDP growing, then the August PCE report might beg to differ: Real spending grew a mere 2.27% over prior year. The fact is, four of the five core GDP sectors have already thrown in the towel. Housing and business CapEx are flatlining, net exports are heading south (thank you, POTUS) and the government sector already is bulging with red ink. So if the vaunted American consumer is now slouching towards stall speed---a trend which has been underway since real consumption spending growth peaked at 4.5% back in February 2015---from whence cometh the stick save for an aging business cycle that is on the verge of rolling over? The answer, of course, is that there will be none. Not from the Fed and not from anyone else because the Fed's massive 10-year long "stimulus" in the form of NIRP and QE did not fix the economy that collapsed in 2008; it just injected it with palliatives that actually aggravated the on-going metastasis below the surface. What the Wall Street permabulls and Keynesian stimulus preachers don't get is that under the current central banking regime, the advancing age of the business cycle does not become her. In mechanical terms, months 120-130 of the cycle (where we are now at the never before recorded mid-point) are far more precarious than months 20-30 because Keynesian policy is a form of dissolute economic living. Accordingly, the longer the stimulus is applied, the more unsustainable debt, speculation and malinvestment builds up throughout the warp and woof of the financial system and underlying economy. Like alcoholism in humans, Keynesian stimulus is a progressive disease that leaves the body economic ever more vulnerable to external shocks, otherwise known as black swans. The heart of the matter is deep and sustained interest rate repression. It means that prior excesses are never ameliorated or purged. They just become the rotten foundation on which new layers of debt, speculative excess and economic "mistakes" are layered upon. So when all five sectors of the GDP (excluding second order change in highly volatile business inventories) are limping and listing toward the flat-line in month #124 of a business expansion, you can be sure that the economy is literally riddled with disease. The investment and spending mistakes fostered by 10-years of artificially cheap debt and the desperate scramble for yield among investment managers eventually overwhelm capitalism's inherent forward momentum.

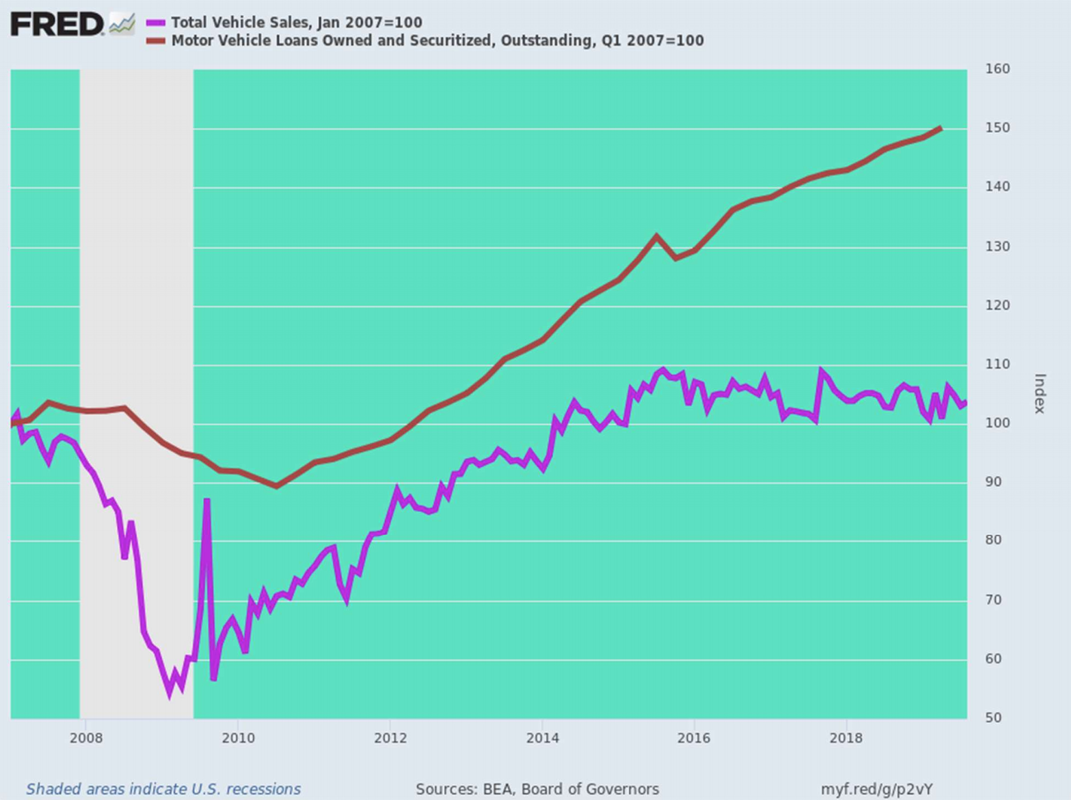

A Wall Street Journal story today nicely illustrates this progressive disease syndrome and is fittingly entitled, "The Seven-Year Auto Loan: America's Middle Class Can't Afford Their Cars".

The jist of the article is that since 2009 the average transaction price of new autos has risen from $30,000 to $40,000 or by 33%. That compares to just a 25% gain in average hourly earnings---a shortfall which would have materially squeezed auto affordability in an honest finance market. But what happened instead is that auto loan maturities were substantially lengthened so that the lagging wages did not cut into loan-financed demand. That is, buyers purchased ever more expensive vehicles at a constant share of wages simply by kicking the debt can further down the road: Walk into an auto dealership these days and you might walk out with a seven- year car loan.

At the same time, the size of the average auto loan has grown by about one-third over the last decade from $24,000 to about $32,000 for new vehicles. So from a debt burden viewpoint, it's a case of "bigger for longer".

It's also a second cousin to Charles Ponzi. What is happening is that the share of auto trade-ins with negative equity has soared from 17% in 2009 to 27% by 2014 and then to nearly 34% at present. Needless to say, owing $5,000 or $7,000 more than a 7-year old vehicle is worth would ordinarily be a huge barrier to getting a brand new ride. The borrower would either need to default on the old loan, thereby causing their credit score to tumble, or reach into savings to pay-off the old loan and potentially have nothing left for a new car down payment. But to paraphrase the late night TV pitchman: Negative equity? No problem! That's right. What the industry debt machine is doing is simply rolling negative equity into the new vehicle loan. That means, in turn, the new loan advance rate is often 115% or even 135% of the transaction price of the new car being purchased. Do that a couple of purchase cycles, of course, and even Charles Ponzi would be impressed. Indeed, the WSJ story includes an anecdote of how a 22-year old minimum wage worker got himself a new Honda Accord in just that way. We are kind of partial to this story because it happened in the namesake of our long ago home town in Flyover America and involves a transaction so devoid of common sense that back in the day it would have been considered sheer lunacy: Deven Jones walked into the Rolling Hills Honda dealership in St. Joseph, Mo., about three years ago after a salesman emailed him and said he might be able to buy a new car for less than $400 a month.

A 133% loan-to-value ratio for 1.9% interest? Exactly what alien economic planet have we landed upon!

As the WSJ story further noted, we have now reached the point where just 18% of US households have enough liquid assets to cover the cost of a new car. In fact, if the median income U.S. household ($63,000) were to employ even a moderately conservative financing and take out a 4-year loan with a 20% down payment while keeping the interest cost under 10% of gross income---a standard ratio---it could afford a new car worth just $18,390. So you better make that a mountain bike with a battery-pack, instead. Nor is that the extent of the impairment. Since 80% of households must now plunge deep into debt with loans so large and burdensome that they actually destroy the borrowers equity, the auto sales business has been transformed as well. Dealers now make more money from financing cars than they do from selling them! So far this year, dealerships made an average of $982 per new vehicle on finance and insurance versus $381 on the actual sale, according to J.D. Power, a data and analytics company. A decade earlier, financing brought in $516 per car and the sale made dealers $837.

Needless to say, where all this cheap debt comes from is not hard to find. The Fed's ultra-low rates functioned as a rolling bailout for the entire auto industry. Fund managers desperate for yield lined up around the block and back for securitized auto loans.

Last year, investors bought a record $107 billion of bonds backed by cars, causing total outstandings to rise to $264 billion compared to just $100 billion in 2009. Moreover, the securitized portion of the Auto Debtberg is only the tip of the thing. Overall, auto debt outstanding now totals $1.3 trillion compared to $740 billion in the immediate aftermath of the financial crisis. And not surprisingly, in some large dealerships which push loans to anyone who walks into the showroom and can fog a rearview mirror, some 40% of employers are in the loan collection business. A further anecdote in the WSJ story reminds where the auto Debtberg ultimately leads: In mid-April, a representative who handles the most-difficult cases called a past-due borrower to iron out payment on a 2018 Toyota RAV4. The borrower had struggled to keep up with a payment of more than $800. The car already had been repossessed from the borrower once.

Actually, where it really leads on an aggregate basis is to a debt encumbered dead-end.

Thus, total US light vehicle sales plateaued at about 17 million units annualized in late 2006-early 2007. They plunged as low as a 10 million rate during the Great Recession and market disorder owing to the bankruptcy of GM and Chrysler, but then fought their way back to the 17 million level by May 2014. They have pretty much flat-lined around that level ever since. But not so with the above referenced Auto Debtberg. By May 2014 auto debt outstanding (brown line) was already 20% higher than the January 2007 level, and then it has just kept climbing, reaching 150% of its 2007 level in Q2 2019. What that means is that for the last five years auto sales have flat-lined (purple line), even as auto debt has continued to soar. In short, during the current so-called recovery cycle it took a 50% increase in auto debt outstanding simply to get annual sales back to the 17 million marker set 12 years ago in January 2007. That's the stimulus disease at work. When the next recession inexorably arrives, far more auto-borrowers will be under water and will be unable to pay when their jobs or incomes dry up. Yet the amount of auto paper in harm's way will be 50% larger.

So we return to the larger proposition. Our Keynesian stimulus preachers never, ever look under the balance-sheet hood. They are totally flow-obsessed.

So are cars still selling at the respectable 17 million rate represented by the purple line after 2014 in the chart above? Why, yes they are. Is the Auto Debtberg heading skyward? Apparently, you are not supposed to ask.

This article was reprinted with permission from David Stockman's Contra-Corner.

David Stockman began his career in Washington as a young man and quickly rose through the ranks of the Republican Party to become the Director of the Office of Management and Budget under President Ronald Reagan. After leaving the White House, Stockman had a 20-year career on Wall Street. Stockman is an Advisory Board member for the Ron Paul Institute for Peace and Prosperity.

Turkey's Erdogan has again promised to invade Syria and establish a "safe zone" extending 20 miles into Syrian territory along 300 miles of Syria/Turkey border. What will happen to the US-backed Kurds, who Erdogan calls "terrorists," that live in that area? What about US military installations that may exist in the "safe zone"? For that matter, what will Putin and Rouhani have to say about Erdogan's threats?

|

Archives

May 2024

|

RSS Feed

RSS Feed